What is it?

We believe that the inclusion of nuclear and natural gas as “green” technology in the EU taxonomy could have important implications for energy and utility companies in the Eurozone and for future Canadian and US regulation where both play larger roles in their respective economies.

- The EU Taxonomy is a classification system that defines environmentally sustainable economic activity under EU law

- The Taxonomy came into law in July 2020 with specifics now being ratified (referred to as “delegated acts”)

- One section that is yet to be determined was the designation of nuclear and natural gas as “green” activities given their role in the transition away from higher emitting energy sources

Where do we stand?

- The European Commission announced expert consultations at the start of 2022 to define the criteria for the inclusion of natural gas and nuclear activities as sustainable

- Natural gas inclusion entails a variety of requirements, mainly aimed at ensuring natural gas plants are being developed only to replace higher emission sources (mainly coal)

- Nuclear inclusion covers activities such as R&D, maintenance of existing assets, and construction of new nuclear plants

What is our view?

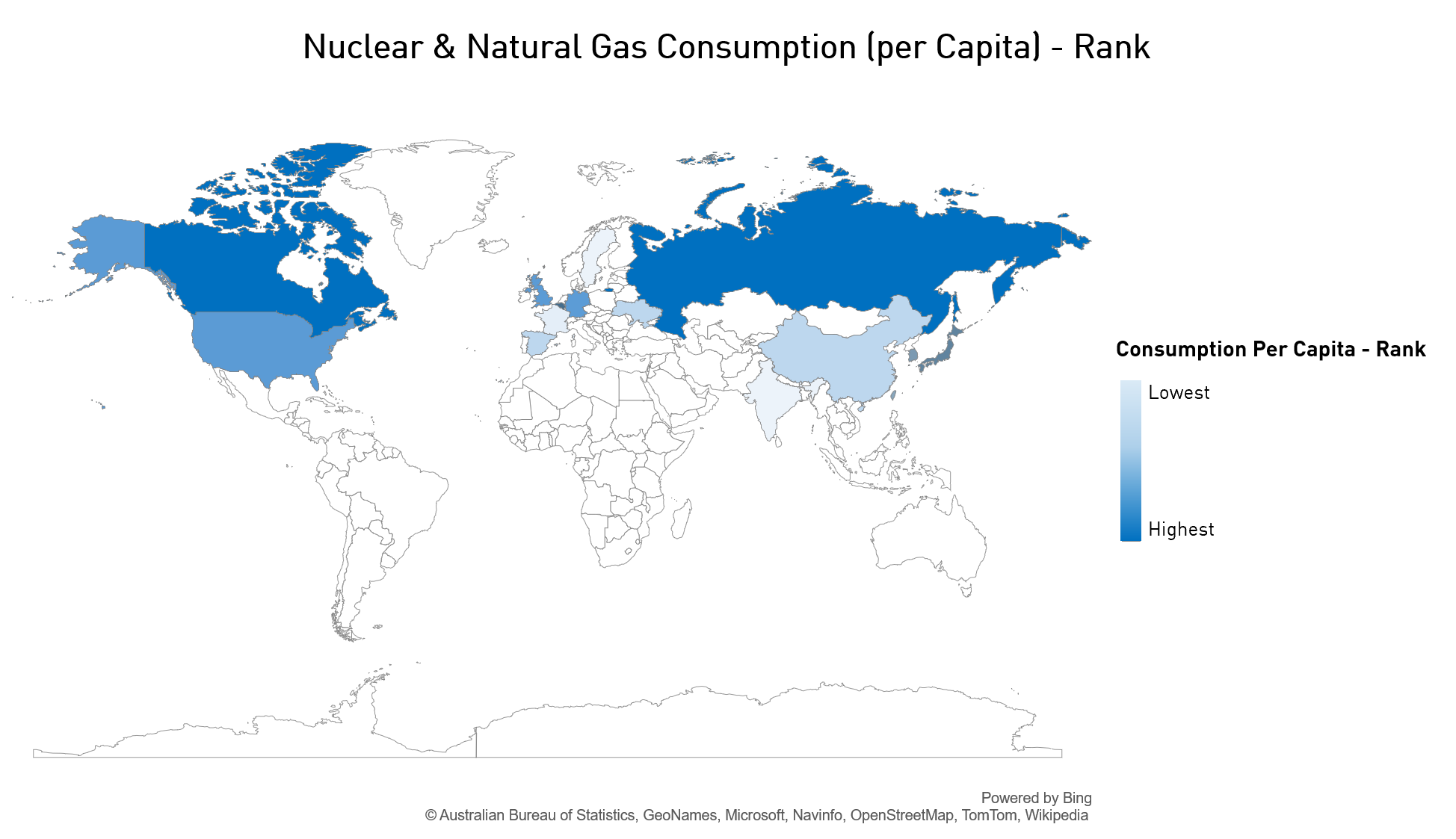

The EU’s treatment of natural gas and nuclear could have wide-ranging implications for Eurozone issuers and similar Canadian and US policies. Policy setting could have larger-scale impacts in Canada and the US where both natural gas and nuclear energy dominate consumption and energy exports.

- We view the inclusion of natural gas and nuclear as positive developments but the regulation needs to place a greater emphasis on both technologies as transitory, not permanent

- Specific considerations regarding natural gas include:

- Defining natural gas as a “green” technology may slow the transition to lower-emitting sources such as renewables and biofuels, even if it helps replace coal power

- The current proposal does not place enough emphasis on natural gas as a transition fuel and may result in member states locking in natural gas technology for decades instead of building future capacity in renewables

- Permanent adoption of natural gas as “green” would undermine Europe’s pathway to net-zero which requires a decrease in natural gas consumption to 13% by 2030 and 3% by 2050 (from 22% today).

- Still much to be debated over nuclear:

- Despite being a near-zero emissions technology, nuclear must meet the EU Taxonomy’s “Do No Significant Harm” threshold which will require member states to show credible, long-term plans for waste treatment

- The proposal opens the door for Small modular reactor technology (an area of R&D that Canada has been a leader in

As Eurozone members debate the inclusion of natural gas and nuclear as “green”, we think the implications go far beyond the EU. The EU Taxonomy is the “standard setter” for regulations in other jurisdictions, so the treatment of natural gas and nuclear has important implications for energy-dominant economies and the financing of activities related to both fuel sources (a topic we discuss here). Canada ranks amongst the top natural gas exporters in the world and is consistently a top natural gas and nuclear energy consumer. Energy, utility, and financial issuers could face challenges as regulation comes into force.

The treatment of natural gas and nuclear is a trend we will continue to watch closely, considering how changes in definitions from “green” to “transitory” will impact the US and Canada.