Executive Summary

- We do not believe "bonds are dead" but that the environment warrants a different asset class approach.

- February reminded investors that rising yields could quickly wipe-out coupon income for a traditional bond portfolio.

- We believe the risk-reward favors fixed income strategies that focus on credit risk rather than interest rate risk.

During February, there was a sharp increase in yields, once again bringing into question whether bonds can play a useful role in a diversified portfolio. There are concerns around both the low level of income bonds provide as well as whether they can provide capital preservation. Only last week, Warren Buffett commented "Bonds are Dead" in his annual Berkshire Hathaway newsletter. We do not believe "Bonds are Dead" but believe that the traditional approach to bonds will not provide investors with what they need looking forward. We think a non-traditional approach to bonds is warranted rather than abandonment of the asset class altogether.

Re-think your fixed income allocation, do not abandon it. As the return outlook for fixed income has deteriorated, there can be a temptation to reduce that allocation and add to other higher-return asset classes. While this may improve expected returns, it also entails an increase in the overall risk. Depending on the investment chosen, this may lead to increased mark-to-market risk, impairment risk, liquidity risk, or a combination of the above. Now is probably not the correct phase of the cycle to be adding to risk. A more prudent approach is not to abandon diversification but rather to look at ways of reconfiguring the portfolio's segments to improve the expected return per unit of risk. Given the outlook, we believe the fixed income allocation is a great place to start.

Now is the time to get creative with your fixed income allocation. In response to a pandemic, last year central banks used a host of stimulative measures to keep economies afloat. In general, fixed income portfolios performed exceptionally well year-over-year as historically low-interest rates sent bond prices soaring. 2021 has followed a different path, and bond yields increased significantly in February. The US 10-year Treasury yield rose from 1.07% at the end of January to 1.54% during the month (Source: U.S. Department of The Treasury). While this was a significant move, yields still sit at low levels by historical standards. Without the tailwind of falling rates, a simple "coupon clipping" approach to fixed income will not work. It does not take much of an increase in yields to wipe out a full year's income. For example, a 10-year Government of Canada Bond can only sustain an increase of 14 bps before the yield for the year has been fully eroded.

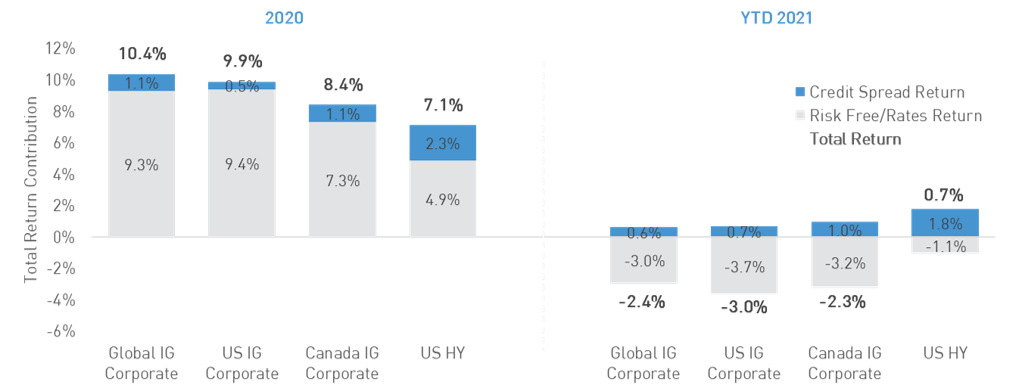

In this environment, we believe you should focus on strategies with less exposure to interest rates. There are typically two different risks within a bond portfolio – interest rate risk and credit risk. Interest rate risk or "duration risk" reflects compensation for uncertainty around the path of future interest rate levels. For traditional bond funds, this risk factor tends to drive most of the return. Last year bond funds benefitted from the fall in interest rates. To date, 2021 has been the mirror image, with fixed income returns weighed down by a negative contribution from the move higher in yields (see chart). That pattern will persist over time if interest rates continue to move higher. Rather than banking on yield being stabilizing or moving lower once again, we believe investors are better served to allocate to strategies that focus on a different risk factor – credit risk.

In 2020, falling yields boosted fixed income returns. Higher yields this year have pushed bond fund returns negative.

Strategies that focus on taking credit risk generally have a more attractive risk-return outlook. When an investor assumes credit risk, they are not considering the direction of interest rates but rather earning a return from a probability of default. Although credit spreads – which measures the compensation investors received for assuming this default risk – are modest by historical standards, there are several areas of the market where opportunities still exist. For example, in recent months, we have been allocating capital to the EUR-denominated corporate bond market, which looks attractive on a relative value basis versus Canada and the US. We have been overweighting sectors such as Financials, Telecoms and Real Estate where we see the best risk-reward. Moreover, credit markets are inefficient, providing opportunities for us to add considerable value in excess of a coupon clipping return. An active, tactical approach to fixed income focusing on a broader universe of bonds is at the center of our investment approach.

The move higher in yields in February demonstrated the value of having a more comprehensive tool kit. It is tough to predict the future path of interest rates, but we strongly believe that investors are not adequately compensated for taking interest rate risk at present. Our fixed income strategies have the tools to reduce or eliminate duration risk, which is a key advantage in delivering on investors' risk-return objectives. We also have the expertise available to identify and invest in the global credit markets' best risk-adjusted areas. Exploring opportunities in global credit (with the currency risk managed) means we can build more diversified portfolios with a wider selection of investments to choose from. Our highly active investment style means we can take advantage of market dislocations to reposition portfolios quickly to add value and manage risk. Finally, we manage several strategies that can short-sell corporate bonds to benefit our investors when we identify parts of the overvalued market. While the outlook for traditional fixed income investments is challenged, we see plenty of opportunity within our area of expertise – credit – and are upbeat on the opportunity set looking forward. We welcome the opportunity to discuss how our solutions can help you reach your investment objectives in this environment.