Back

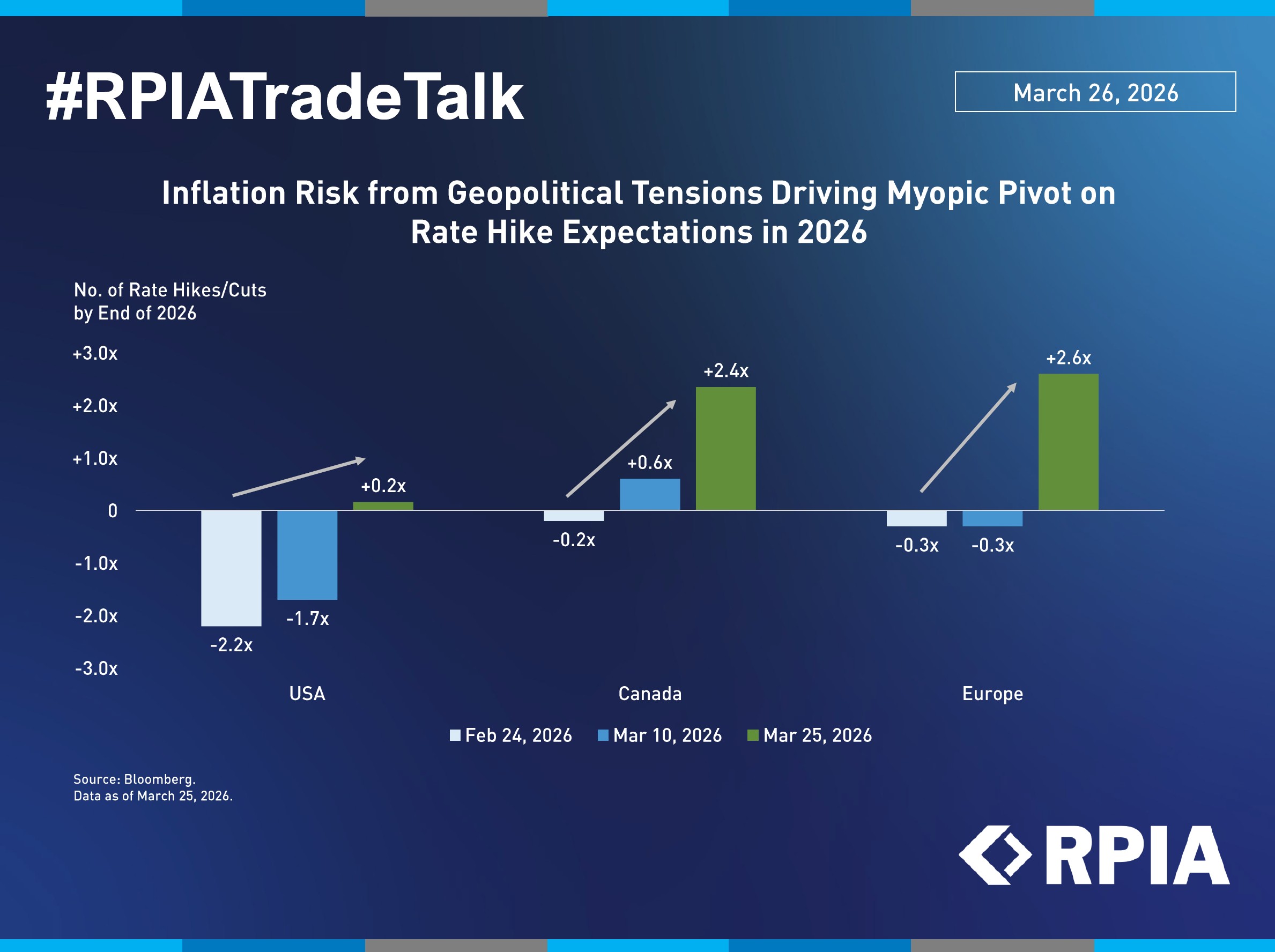

Inflation Risk from Geopolitical Tensions Driving Myopic Pivot on

Rate Hike Expectations in 2026

Inflation risk has been the dominant theme over the past two weeks, with market sentiment increasingly shaped by rising geopolitical tensions and a growing realization that the current energy shock may prove more persistent than initially expected. As a result, policymakers are focusing more on anchoring inflation expectations, even as the growth outlook becomes more fragile. Just one month ago, US, Canadian, and European markets were pricing varying degrees of rate cuts; however, those expectations have shifted sharply, with energy-importing regions like Europe now pricing in as many as 2.6x rate hikes vs. a -0.3x cut only two weeks ago.

While we acknowledge the magnitude of the recent upward move in short-term interest rates, we don't think it considers the full picture. We continue to believe that demand destruction, evolving employment trends, and slowing growth will ultimately shape central bank policy later this year. We remain constructive on duration, particularly in the US and Canada, and would look to tactically add exposure on further weakness.